Table of Content

That means there’s less risk for the lender and you’ll get a better rate than you would if it were a second mortgage. The more equity you’ve built in your home over the years, the more you may be able to borrow against it with the help of a cash-out refinance loan. Home equity loans and home equity lines of credit are also an option to utilize your home equity. If an equity loan is used for anything else – to pay off credit card or student loan debt or personal use — it is not tax deductible. The reduced interest rate means your monthly payments should be lower and you make only one payment each month. HELOCs are credit lines, meaning you use as much of a pre-approved loan amount as you want, when you want.

Jeanne is a former NerdWallet writer focusing on credit, debt and loans. She has covered financial topics for more than 20 years, including stints at Fortune and Money magazines. Your home’s equity could be one of the most valuable things you own. You may work 15 – 30 years to pay it off, so be cautious when you use it.

Best for Flexible Repayment Terms

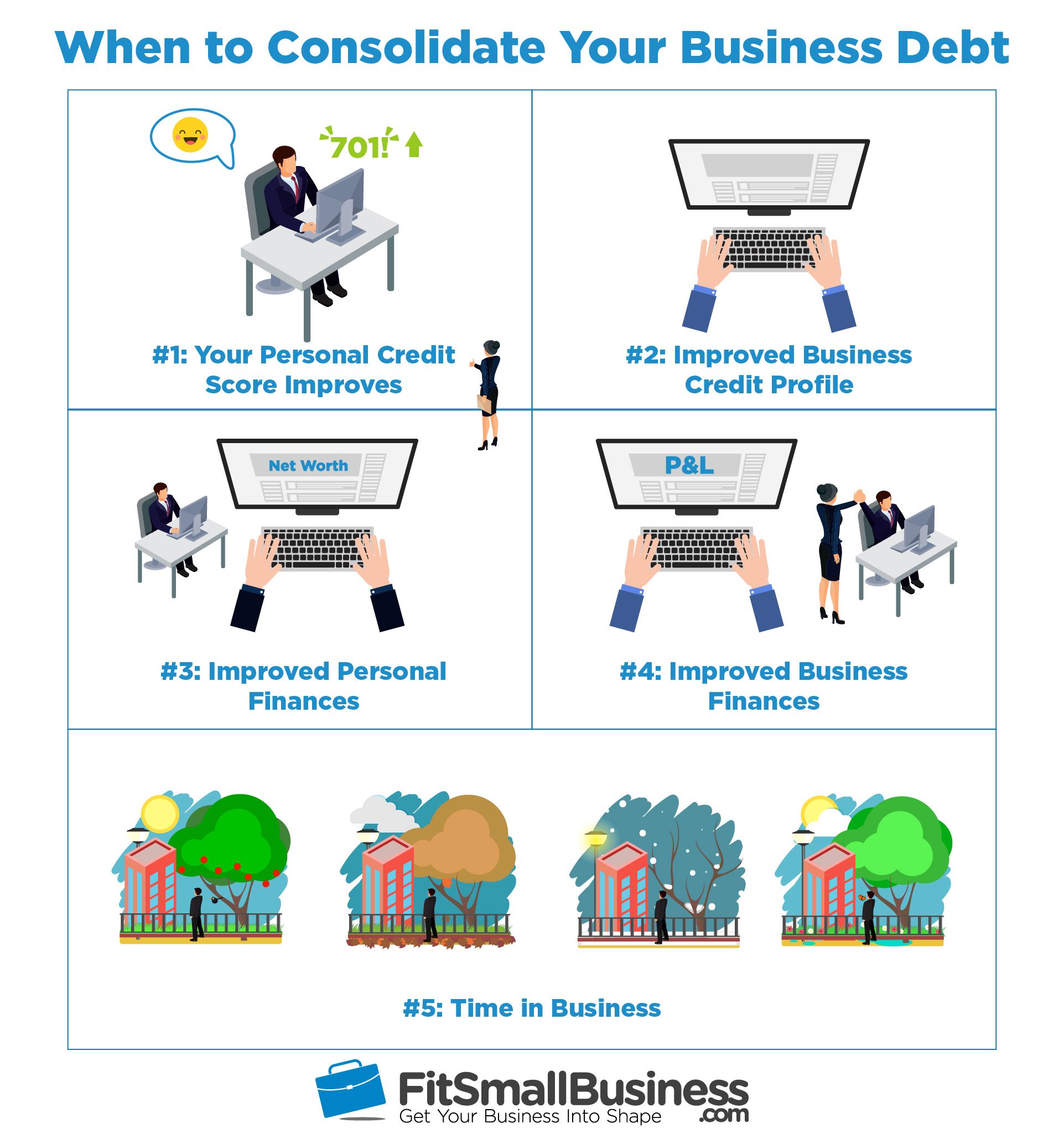

Understanding your options is critical in today’s unpredictable world. You typically borrow the greater of $10,000 or 50% of your vested account balance up to $50,000, and you generally have up to five years to repay it. To determine which consolidation method best fits your life, consider talking to an expert such as a credit counselor. But as long as you make the payments on time and don’t go right back into debt, The results for your credit should be positive. In others , the lender may require that they send the funds directly to your creditors. A consolidation loan is not the only type of financing you can use to pay off debt.

If you don’t meet the credit score or income requirements, you may consider applying with a co-applicant, who will be jointly responsible for paying off the loan. It’s important to note that a co-applicant isn’t the same as a co-signer, who assumes responsibility for the loan if the main applicant cannot pay. SoFi and most other debt consolidation lenders do not allow co-signers on their personal loans. For example, let's say you owe $10,000 in credit card debt with an average APR around 22%, and you're currently paying $400 every month to meet the minimum payments. It would take you a whopping 184 months to pay off this debt, and you'd end up paying $8,275.44 just in interest. Now suppose you got approved for a $10,000 consolidation loan with an interest rate of 11%.

SEARCH DEBT.COM

Beware, if a credit facility stays open, even unbeknown to you, you could continue to be charged monthly or annual fees. Similar to a home equity loan, a HELOC also gives you access to funds through your home equity. However, instead of receiving funds as a lump-sum payment, you’ll have access to a credit line you can use as needed, and reuse as you repay your balance during the draw period. You’ll also only pay interest on the amount you borrow, not the entire approved amount. If you have sufficient equity in your home, typically at least 15-20%, you may be eligible to borrow up to 85% of your equity. Funds are disbursed as a lump-sum payment, which you can use to repay high-interest debts, and interest is owed on the full loan amount.

The Ask Experian team cannot respond to each question individually. However, if your question is of interest to a wide audience of consumers, the Experian team may include it in a future post and may also share responses in its social media outreach. If you have a question, others likely have the same question, too. By sharing your questions and our answers, we can help others as well. Take a financial inventory and see if you can battle your debt without using methods like debt consolidation. The main thing here is to stay disciplined and not spend more than you truly can afford.

Debt Consolidation

Consolidating your debt could possibly have a positive impact on your debt-to-income ratio by reducing the amount of your monthly payment. There are a couple reasons you might opt for a HELOC debt-consolidation loan rather than a standard home equity loan. On the other hand, HELOCs usually have adjustable interest rates, which can make them unpredictable and making interest-only payments greatly increases your out-of-pocket costs over time. For those struggling with high interest rates and juggling several monthly payments, an unsecured credit card or personal loan could be a better alternative for debt consolidation.

In addition to offering flexible loans that are available for three- to six-year terms, Marcus also assists debt consolidation borrowers by offering direct payment to third-party creditors. Debt consolidation loans are best used when you have long or open-ended term debt with high interest rates due to the nature of how they are structured. Consolidation loans will have relatively short, specified terms—typically ranging from one to seven years. This means that you could pay off balances sooner than you would with loans featuring longer terms or revolving types of debt, such as credit cards. This will help you determine exactly how much to borrow if you choose to consolidate with a home refinance loan.

Our team of friendly, professional lending Experts are ready for your call to determine if a debt consolidation refinance is right for you. That monthly debt payments don’t exceed 50% of a homeowner’s monthly gross income. If you’ve ruled out other options, weighed the pros and cons of consolidating with home equity and determined it’s the viable path, then it’s a choice of a home equity loan or a HELOC. A homeowner with shaky finances shouldn’t move unsecured debt that can be erased in bankruptcy to secured debt that can’t. Unless you have a very solid income and live in an area where home prices are consistently rising, replacing consumer debt with an equity loan is probably not a good idea.

Review the lender’s customer service resources and read reviews from past and current borrowers to make sure it’s a good fit. Within each category, we also considered several characteristics, including available loan amounts, repayment terms, APR ranges and applicable fees. We also looked at minimum credit score requirements, whether each lender accepts co-signers or joint applications and the geographic availability of the lender. Finally, we evaluated the availability of each provider’s customer support team. LightStream is a consumer lending division of Truist—which formed following the merger of SunTrust Bank and BB&T. The platform offers unsecured personal loans from as little as $5,000 up to $100,000.

If you have significant high-interest debt, using your home equity to pay it off will likely result in a lower interest rate. Reducing the interest rate you pay on your debts will help you pay off balances faster since more of your payments will go towards the principal versus interest. Taking on a home equity loan or HELOC for debt payoff has its advantages, but it also comes with risks. Experts also suggest exploring alternatives before you use your home equity to consolidate debt. While using these services is easier than searching for debt consolidation loans, many of these companies charge steep fees for their work and may not always be successful in their efforts. A good way to find the best personal loans is to compare multiple lenders.

Usually, a home loan refinance is the only way to add someone to a home loan. While you are refinancing your home loan to consolidate debt, take the opportunity to add someone onto your home loan if it’s what you’ve been looking to do. It’s important to remember that you’ll need to add the other person onto the Title Deed of the property if you want them to be an owner of your home. Typically, no – paying out your credit card or Buy Now Pay Later facility won’t automatically close the account down. Often, you will be required to tell the credit provider you wish to close the facility.

No comments:

Post a Comment